Let’s be honest—budgeting can feel intimidating, especially if numbers aren’t your thing. But here’s the good news: building a budget is one of the most empowering steps you can take to gain control over your money. And no, you don’t need to be a math genius to do it.

Why Budgeting Matters (Even If You Hate It)

Budgeting helps you:

- Understand where your money is going – Ever wonder where your paycheck disappeared to? A budget reveals those spending habits.

- Take control of your spending – With a plan, you can cut unnecessary expenses while keeping the things that truly matter.

- Achieve financial goals – Want to pay off debt, save for a trip, or build an emergency fund? A budget keeps you on track.

- Reduce stress – Knowing your money is handled can ease financial worries.

Step 1: Calculate Your Monthly Income

Start by figuring out how much money you have coming in each month. Include:

- Salary or Wages: Your take-home pay after taxes.

- Side Hustles: Freelance work or gig income.

- Other Income: Child support, government benefits, dividends.

What if Your Income Varies? If your income fluctuates, base your budget on an average of the past 6-12 months and lean towards the lower end to avoid overspending.

Step 2: List Your Fixed and Variable Expenses

Now, break down where your money goes.

Fixed Expenses:

- Rent or mortgage

- Insurance

- Loan payments

Variable Expenses:

- Groceries

- Dining out

- Entertainment

Track Your Spending: If you’re unsure of exact numbers, track your expenses for 30 days using apps like Mint or YNAB.

Step 3: Categorize Your Expenses

Group your expenses into categories for clarity:

- Housing: Rent, utilities

- Transportation: Gas, car payment

- Food: Groceries, takeout

- Savings: Emergency fund, retirement

This makes it easier to see where you can cut back.

Step 4: Set Financial Goals

Why are you budgeting? Define your top 2-3 goals, like:

- Build a $5,000 emergency fund

- Pay off $2,000 in credit card debt

Why It Matters: Having clear goals helps you stay motivated.

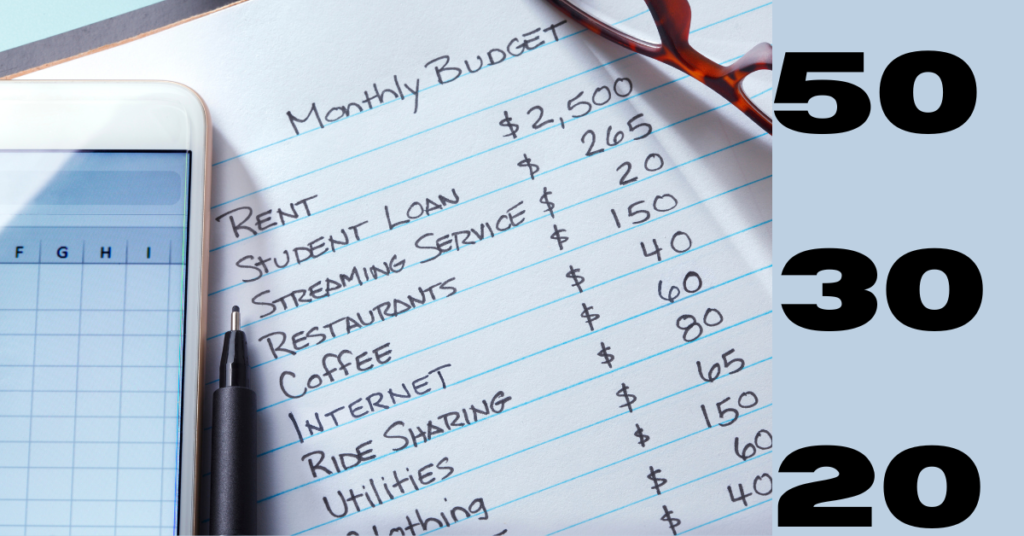

Step 5: Try the 50/30/20 Budgeting Rule

A simple way to structure your budget:

- 50% for Needs: Housing, food, utilities

- 30% for Wants: Hobbies, dining out

- 20% for Savings/Debt Repayment: Emergency fund, retirement, loans

If your “needs” exceed 50%, look for adjustments in the “wants” category.

Step 6: Track and Adjust Monthly

A budget isn’t static. Review it monthly and adjust based on:

- Changes in income

- Unexpected expenses

Use apps like Mint to simplify tracking.

Step 7: Automate Savings and Payments

Automation makes budgeting effortless:

- Set Up Auto-Transfers: Move money to savings automatically.

- Automate Bills: Schedule payments for rent, loans, and utilities.

Step 8: Be Kind to Yourself

Budgeting takes practice. If you overspend one month, adjust and move forward. It’s about progress, not perfection.

Final Thoughts

Creating a budget doesn’t have to be complicated. By following these steps, you can take control of your finances and reduce stress. Remember, it’s not about restriction—it’s about freedom. Where will you start today?